Recently, Reserve Bank of India (RBI) Governor Shaktikanta Das has raised concerns over the rise in the related-party transactions. “Of late, several instances of related party transactions without following ‘arms-length’ principle and established transfer pricing mechanism have been observed,” the RBI Governor said.

There have been instances of diversion of funds and / or transfer of profits to connected parties through various means – intra-group loans on favourable terms, over or under invoicing of transactions, asset transfers without fair valuation, Das said.

Further, the RBI Governor said auditors must be careful about such related-party transactions. “Auditors need to identify and thoroughly scrutinize related or connected party transactions to ensure that there is no undue transfer of income or assets” he added.

Investigations by the government agencies such as Enforcement Directorate (ED) revealed that the related-party transactions were involved in most of the loan fraud cases.

For instance, SA Rawther Spices Pvt Ltd is one such case whose assets worth Rs. 145.26 crore was attached by ED in September this year under the provisions of Prevention of Money Laundering Act, 2002 (PMLA). Money laundering investigation conducted by ED has revealed that SA Rawther Spices Pvt Ltd obtained multiple loans, and used the same to export goods mostly to related parties and the export proceeds were never realized in India.

In our view, the banks should have a dedicated system to carry out comprehensive credit risk assessment of large-value accounts and its related entities. Amukha’s Market Intelligence Unit (MIU) is one such application that fits the bill.

MIU performs complete 360-degree credit risk assessment of the borrowers to help the banks to identify accounts with fraudulent behavior both at the time of pre-onboarding stage and during the monitoring stage.

Here, we are presenting the use case of MIU from the perspective of related-party risk.

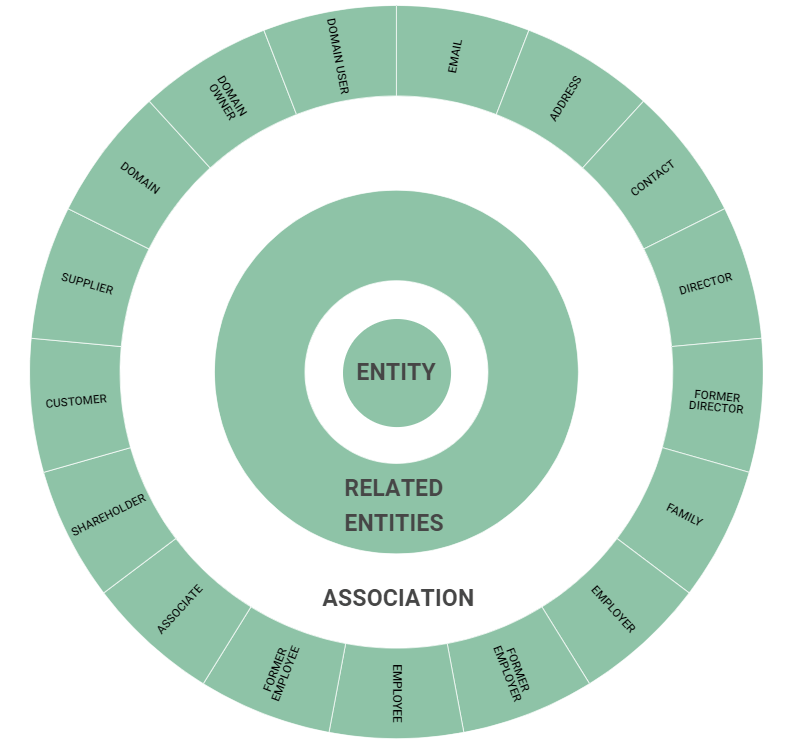

#1. MIU application identifies the Related Parties based on the association with the borrower entity.

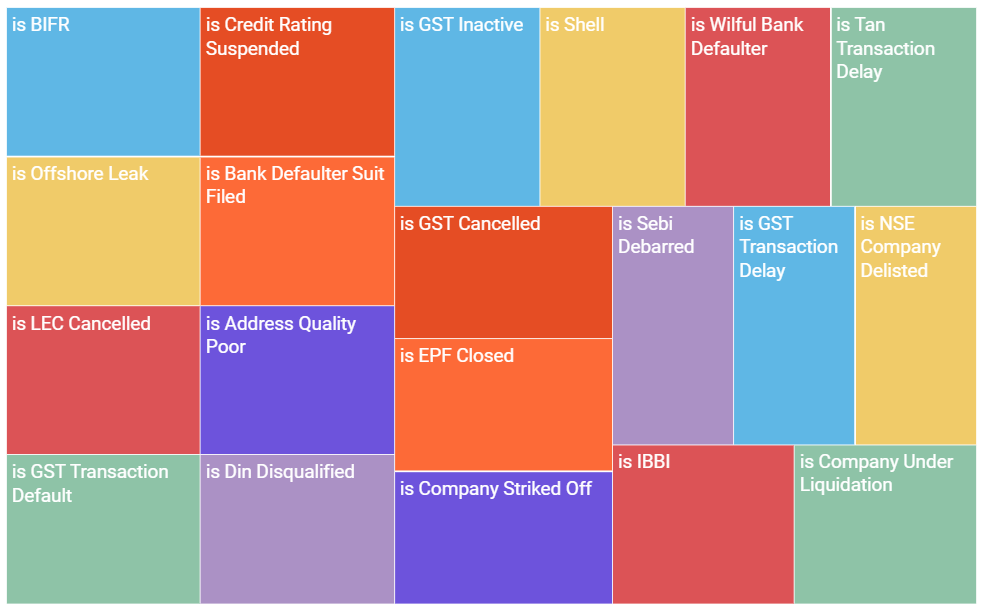

#2. Amukha application screens both the borrower entity and its related parties on 60+ negative alerts. Some of the negative alerts with severe severity are highlighted below.

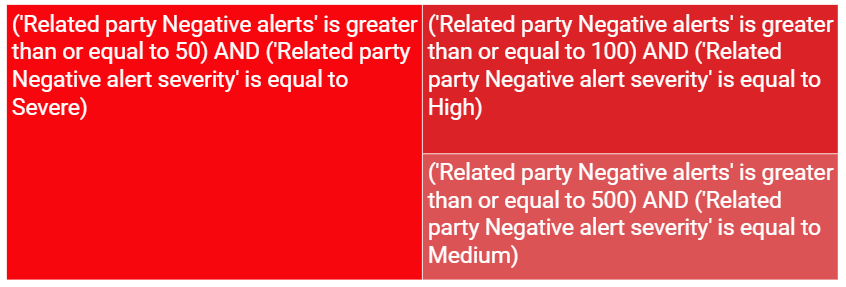

#3. MIU application measures the risk based on 10+ business rules which captures the severity and volume of negative alerts for the borrower entity and its related parties. Some of the business rules with -5 score intensity are shown below:

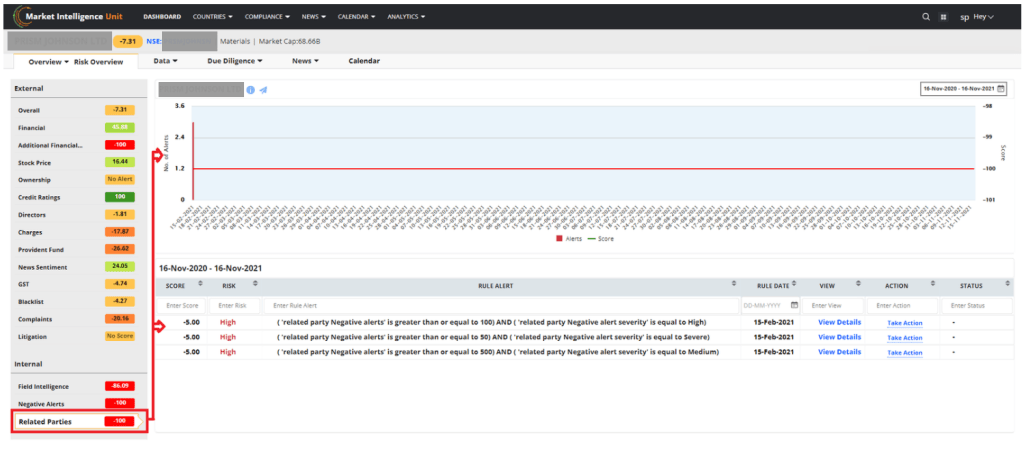

4. The output of these business rules is used to arrive at the Negative Alert Risk Score for both the borrower entity and its related parties. We have highlighted Related Parties module with a score trend chart and business rules for one company below:

MIU application has the capability to identify related parties, screen such entities on negative alerts, measure the underlying risk and thereby help the banks to take appropriate decisions on accounts with fraudulent behavior.

To know more about Amukha MIU application, please get in touch with us at [email protected].